tel

:+86 - 17718123415

E-mail

:info@sailsolaress.com

Overview

Effective May 1, 2026, the European Investment Bank (EIB) and the European Investment Fund (EIF) introduced a new set of financing exclusion rules for power conversion equipment from designated “high-risk regions.” This policy covers solar inverters, wind turbines, and energy storage PCS inverter equipment, constituting a non-tariff trade barrier based on capital access rather than a direct import ban. Combined with Article 28 of the Net Zero Emissions Industries Act (NZIA), which came into effect at the end of 2025, these two rules together raise the market entry barriers for Chinese inverter and energy storage companies to enter the European distributed and large-scale renewable energy sector.

1. Core Terms of European Investment Bank/European Investment Fund Financing Restrictions

1.1 Scope and Assessment Criteria

The European Commission has designated China, Russia, Iran, and North Korea as high-risk countries due to cybersecurity risks associated with grid-connected power electronic equipment in these countries, particularly those related to remote data transmission.

Product Coverage: All power conversion equipment not eligible for power rating exemptions, including low-power residential inverters, commercial and industrial string inverters, utility-scale centralized inverters, and the full range of energy storage PCS. Wind power converters are also included.

Applicable Projects: All renewable energy projects funded by the European Investment Bank, the European Investment Fund, the European Green Transition Fund, national development banks, and the EU's Cross-Border Cooperation Programme. Projects located in the Western Balkans and North Africa and connected to the EU grid are subject to the same rules.

Entity Identification Criteria: The restrictions apply not only to equipment manufactured in the aforementioned four countries but also to products manufactured by entities owned or substantially controlled by stakeholders in these countries—even if the manufacturing facilities are located within the EU. The European Solar Manufacturing Committee (ESMC) has confirmed that no exemptions will be granted for local production in the EU by Chinese-owned brands.

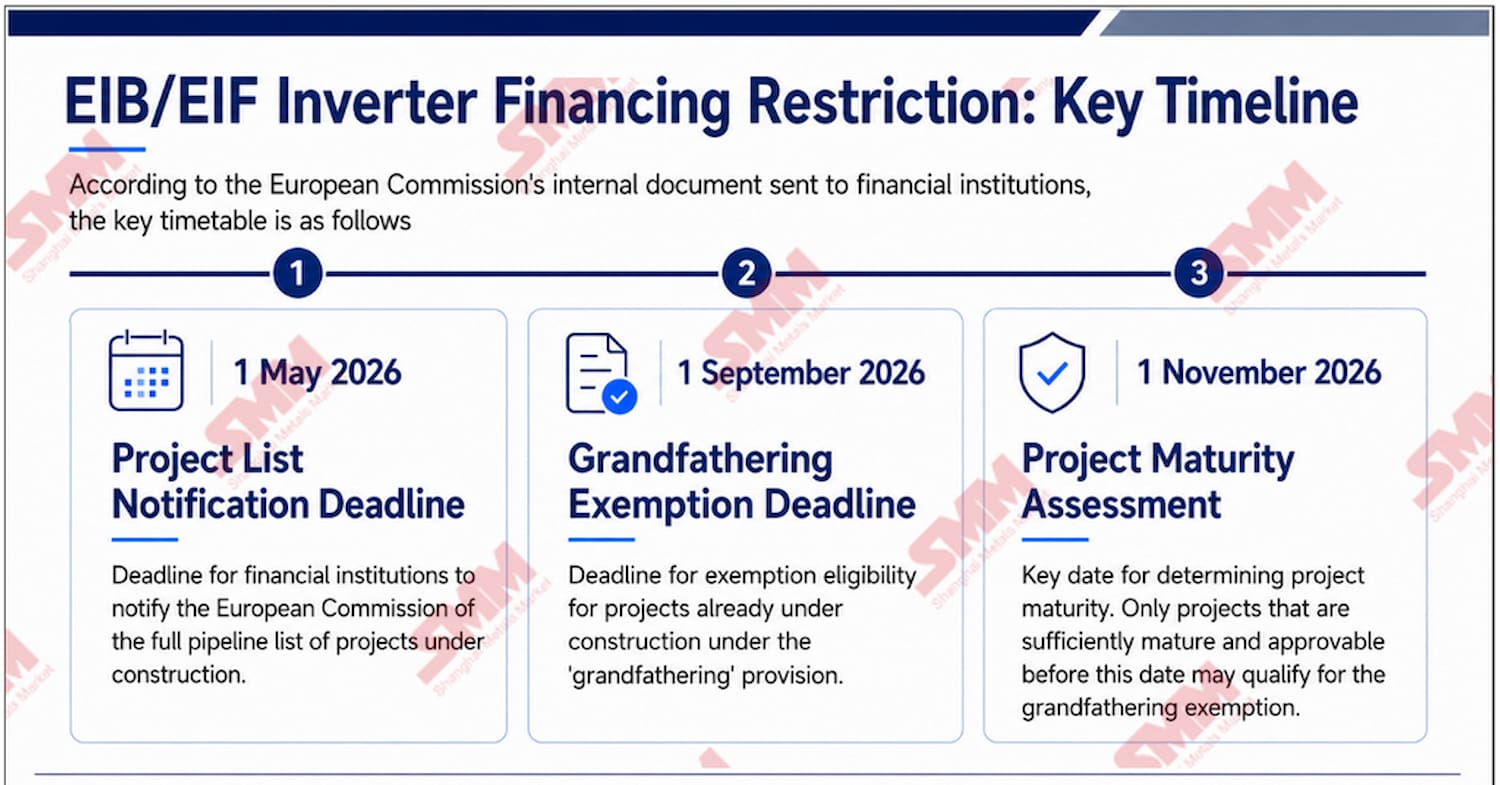

1.2 Mandatory Timeline and Legacy Exemption Provisions

May 1, 2026: Date of official policy entry into force; all participating financial institutions complete a full report to the European Commission on their stock of ongoing and planned renewable energy projects.

September 1, 2026: Deadline for submitting applications for legacy exemption provisions for construction projects.

November 1, 2026: Deadline for final assessment of exemption eligibility. Only mature projects with locked-in equipment supply and no viable alternative hybrid energy storage inverter/PCS supplier space are eligible for long-term exemptions. Early-stage, adaptable projects are not eligible for exemptions, regardless of whether an application has been submitted previously.

April 15, 2027: Deadline for phasing out inverters/PCS from high-risk jurisdictions after non-EU projects are connected to the European grid.

1.3 Supplementary Financing Arrangements and Policy Exceptions

The European Investment Bank has established a dedicated €2 billion renewable energy financing pool specifically for projects using power conversion equipment from non-high-risk jurisdictions. This pool will cover approximately 20% of the EU's solar capacity installed by 2025.

Explicit Policy Buffers: Passive components and core power semiconductors (IGBTs, MOSFETs) used within inverters and PCS are exempt from restrictions. Chinese upstream semiconductor suppliers can continue to supply European inverter manufacturers without funding access barriers.

2. Harmonized Restrictions: Implementation Details of Article 28 of the New Zealand Investment Act (NZIA)

Article 28 of the NZIA, which will come into effect on December 30, 2025, sets out the origin eligibility criteria for EU residential and commercial distributed solar subsidies, and is implemented in parallel with the European Investment Bank's large project financing limits:

- Eight core solar modules require origin verification: polysilicon, silicon ingots, silicon wafers, solar cells, photovoltaic glass, modules, inverters, and trackers.

- Eligibility prerequisites for subsidies:

PV modules must not be assembled in China;

Solar cells and inverters must not be made in China;

At least four of the eight modules must originate from a non-highly dependent third country, with the inverter and cells being one of these four eligible modules.

- Systems that do not meet any of the above rules of origin will be ineligible for EU consumer and business green subsidies. This dual policy framework covers utility-scale ground-mounted PV, stand-alone storage, and residential distributed PV, imposing comprehensive tiered restrictions on Chinese solar power electronics products.

3. Differentiated Industry Impact Assessment

3.1 Short-Term Impact on Each Market Segment

This policy is a financing ban, not an import ban: Chinese inverters and PCS can still be imported and deployed in projects that are entirely privately funded and do not require EU public funding.

Utility-scale ground-mounted PV and stand-alone storage: Most affected. Approximately 20% of the EU's solar installed capacity and over 30% of large-scale storage projects rely on European Investment Bank/European Public Finance. Developers will face higher costs for alternative equipment procurement, longer delivery cycles, and repeated system compatibility testing, thus driving up the overall levelized cost of electricity (LCOE) for projects.

Residential distributed PV: Minimal direct impact, as most residential installations rely on private capital rather than EU institutional loans.

Energy storage PCS market: More severely affected than solar inverters. Large-scale energy storage projects in Europe heavily rely on bank financing, while integrated battery-PCS solutions from Asian manufacturers face the risk of being forced to split modules or change suppliers. Limited local European PCS production capacity leads to a tighter supply gap than for solar inverters.

3.2 Mid-Term Supply Chain Adjustment Trends

Inverter manufacturers in the EU, US, Japan, and South Korea have announced capacity expansion plans, supported by the Net Zero Emissions Industry Act and subsidies from the Clean Industry Agreement. However, the substitution process faces structural headwinds:

High industrial electricity prices, stringent EU Emissions Trading System (EU ETS) carbon costs, and stringent environmental compliance rules have increased manufacturing costs for local European factories;

The EU lacks a complete upstream photovoltaic supply chain, relying on imports for key silicon wafers, cells, and raw materials;

The long investment cycle of asset-intensive photovoltaic production hinders the rapid inflow of capital into local manufacturing.

3.3 Limitations of EU Local Factory Mitigation Measures

The traditional strategy of Chinese companies establishing factories within the EU to circumvent trade barriers is no longer effective under the new regulations. Regardless of the production location, as long as China holds substantial ownership or control, the same financing restrictions will be triggered. Shareholding restructuring and the separation of joint venture brands will face stringent substantive control audits by EU financial institutions.

4. Forward-looking Market Assessment

**Policy Spillover Risk:** The EU's capital exclusion model utilizes financing rules to circumvent formal WTO anti-dumping duties. The UK, US, Australia, and other major renewable energy markets may follow suit, creating cross-regional regulatory pressure on Chinese inverter and PCS exporters.

**Limited Exemption Scope:** Only a small fraction of projects fully locked in before November 2026 qualify for exemptions; Chinese suppliers must accelerate the delivery of existing European orders within the compliance period.

**Upstream Semiconductor Buffer Opportunity:** Unrestricted power semiconductor components remain a stable export sector for Chinese upstream manufacturers, with demand growth closely linked to the expansion of local European inverter production capacity.

**Persistent Supply Gap in 2027-2028:** Structural costs and supply chain constraints will prevent local European production capacity from fully replacing Chinese inverter and PCS supply in the short to medium term, although third-party production in Turkey will gradually meet some demand.

**Implementation Uncertainty:** The European Commission has not yet released formal official regulatory texts, which still contain some unresolved ambiguities, including detailed criteria for identifying substantial controls and the potential expansion of the restricted component list in the future.

--Wondering if your European project will be affected by inverter compliance regulations?

Share your project scale and funding type, and we will provide a compliant configuration plan free of charge.

--How do you select inverters for EU energy storage projects that meet regulatory requirements?

Contact customer service to receive the "Guide to Avoiding Pitfalls in EU Solar-plus-Storage Equipment Selection."

In response to new EU regulations, we are launching localized compliant PCS units, custom inverters without cloud connectivity, and complete energy storage systems available.

We welcome inquiries and opportunities to compare solutions.

Rete IPv6 supportata

Rete IPv6 supportata

Lasciate un messaggio

Scansione su Wechat :

Scansione su WhatsApp :